The strength of consumer spending and household balance sheets has been a bright spot in an otherwise challenging market and economic environment. These factors have helped to keep the economy out of recession and have bolstered corporate earnings, but they have also kept inflation hotter than the Fed might otherwise like, resulting in higher interest rates. For investors and savers, recent consumer data are a reminder that staying the course, and not overreacting to short-term news, is still the best way to build and preserve long-term wealth. What should investors know about the state of consumer finances as market and economic uncertainty continues?

Consumer finances both affect the economy and markets and are affected by them. In the U.S., consumer spending makes up 68% of all expenditures each year, forming the foundation of overall economic activity. How consumers feel about their personal financial situations can thus have an important impact on economic growth, and vice versa. When times are difficult, such as during a recession, consumers naturally tighten their belts which can lead to a spiraling economic slowdown. On the other hand, when the economy and job market are strong, consumer sentiment improves. This in turn supports corporate revenues and profits, spurring hiring and wage increases which can drive further consumer spending. Ideally, this then supports financial asset prices and valuations.

Record Breaking

The economic swings since 2020 are proof of this – from the sudden collapse in consumer spending during the pandemic to the surge in activity during the subsequent rebound, driven in no small part by government stimulus. Fortunately, despite high inflation rates over the past two years, consumer spending has continued to support the economy. This is partly because the average household balance sheet has never been stronger. The Fed’s latest Z.1 report on the Financial Accounts of the United States shows that household net worth climbed to a record level of $154 trillion in the second quarter of the year. This measure includes household assets such as stocks and bonds, bank deposits, defined benefit entitlements, real estate, and more, as well as liabilities such as credit card debt and mortgages.

Household net worth has reached a new record level

Of course, the cost of debt has increased as interest rates have risen over the past year. While the 10-year Treasury yield has fluctuated over the past few weeks, it has been hovering near the highest levels since 2007, even briefly surpassing 5%. This is challenging for those individuals and businesses with new loans or mortgages with average rates above 8%. The silver lining is that many households were able to lock in low rates over the past few years, especially immediately following the pandemic. According to the Federal Reserve Bank of New York, 14 million households refinanced their mortgages during this time and saw an average drop in their monthly payments of $220.

The chart above summarizes the positive net effect on household net worth. It also shows that net worth has more than doubled since the prior 2007 peak. This has occurred despite the never-ending challenges investors faced along the way, including market pullbacks, geopolitical crises, economic slowdowns, problems in Washington, and more recently, inflation, Fed rate hikes, and more. This is a reminder that having a long-term focus has historically been rewarded, regardless of how worrying the short-term headlines may be.

The Consumer

Of course, not all households have benefited equally from these trends. Those with wealth invested in the stock market and real estate have done better since those assets have appreciated significantly. Perhaps more importantly, those that stayed invested and resisted the urge to stray from their financial and investment plans when times were the toughest most likely benefited the most. Fortunately, another bright spot in today’s economic environment is the stronger-than-expected labor market. With unemployment still near historic lows, more Americans have benefited from job security and wage growth, supporting consumer spending even more than in past cycles.

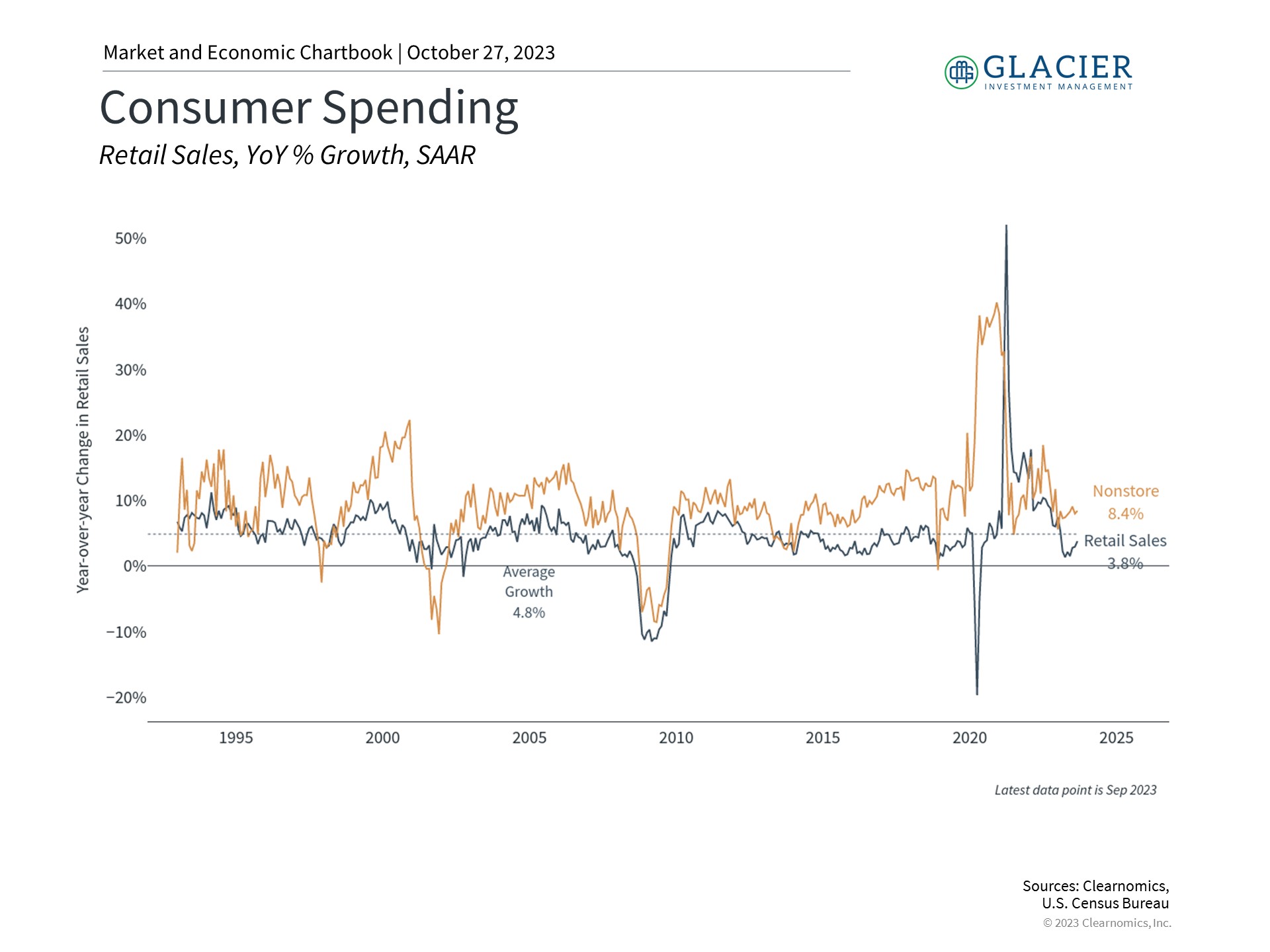

This can be seen in recent retail sales figures. The September data published by the U.S. Census, for instance, were better than economists expected with total retail sales growing 0.7% month-over-month. The previous month’s numbers were also revised up significantly. Other data such as Personal Consumption Expenditures, which serve as an input to GDP calculations and are adjusted for inflation, show similar patterns. There may be headwinds in the near future as consumers draw down on the excess savings of the past few years and if oil prices remain high, but overall, consumers have been remarkably resilient.

Retail sales have picked up

Saving and Investing

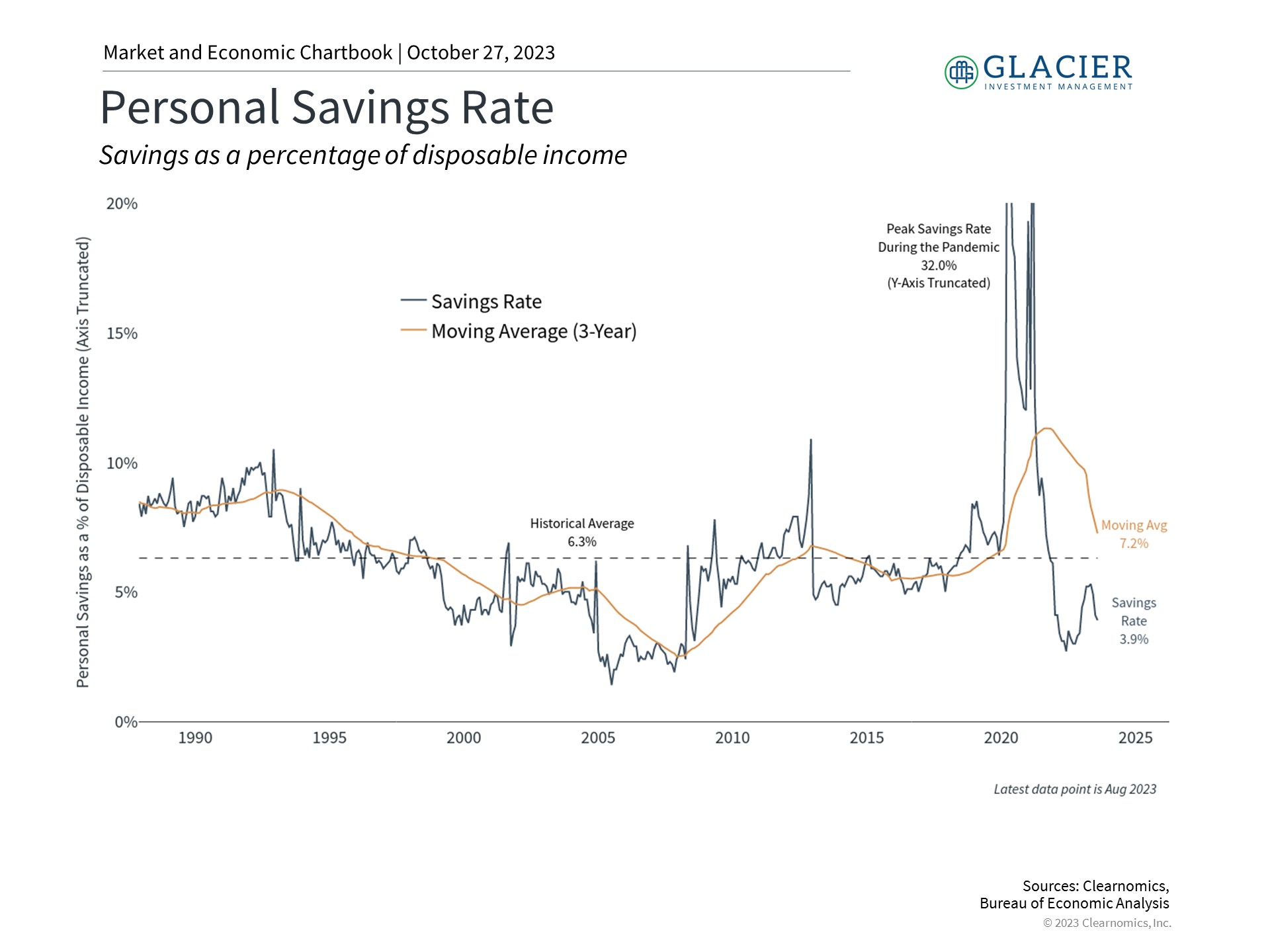

From a financial planning perspective, there is possibly nothing more important than saving and investing enough to meet future goals. This is because, unlike daily market swings, how much you save and how you invest those savings are completely within your control. The accompanying chart shows that savings rates spiked in 2020 but have been low since then as consumers have spent on goods and services. While this has helped support the economy, households will eventually need to tighten their belts. Investors should continue to stick to their long-term financial plans in order to navigate this uncertain environment and benefit from future growth.

Personal savings have declined after a sharp uptick

The Bottom Line

Household net worth has returned to historic highs this year as markets have risen and the economy has been stronger than expected. This is a reminder that all investors should maintain a long-term perspective rather than focus on daily market swings.