Despite the economic uncertainty of the past year, everyday individuals and households have been resilient. Consumer spending has remained steady in the face of high inflation, rising interest rates, housing market challenges, and layoffs in sectors such as tech. While it has helped that the recession anticipated by many investors and economists has not materialized, this fact is partially due to the strength of consumer finances. How do consumer balance sheets look today and how might this impact the economy and markets in the coming year?

Saving for the Future

From a financial planning perspective, there is possibly nothing more important than saving and investing enough to meet future goals. After all, how much you save is completely within your control, unlike the short-term direction of the market. Personal savings and spending are equally important for the broader economy. When times are good and consumers are optimistic about their jobs and financial situations, they tend to spend more. This boosts sales for small businesses and large corporations alike, which then hire workers, make investments, develop new products, and more. This in turn creates new jobs and boosts wages which increase consumer activity further. Thus, how consumers feel is an important economic indicator for investors to consider across business cycles.

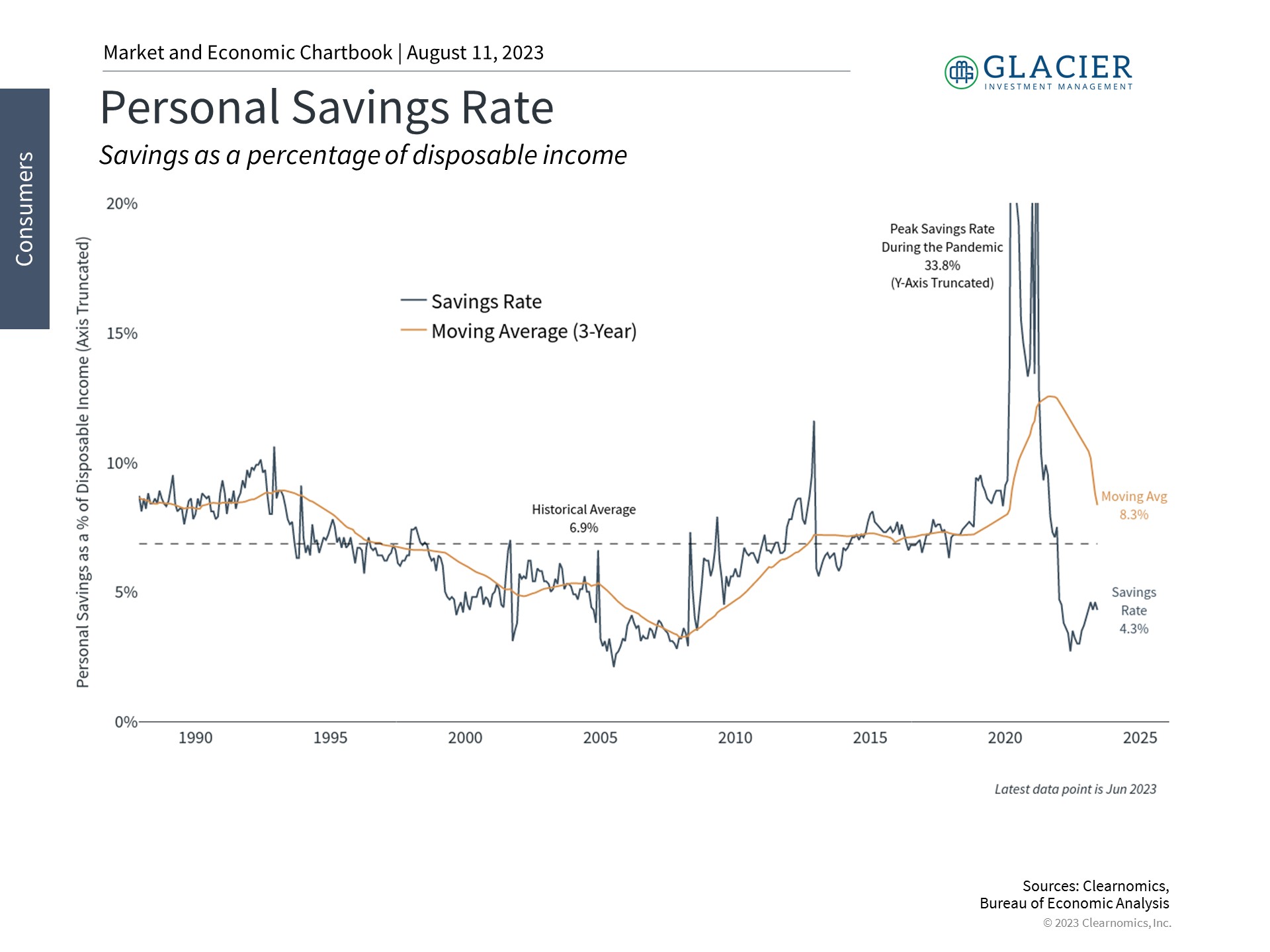

Personal savings have helped to cushion consumer finances

During the pandemic, consumer spending plummeted which led to record savings rates from early 2020 through much of 2021. At its peak, consumers in aggregate saved over one-third of their paychecks, an unprecedented rate that is seven times the historical average. Although this occurred under difficult personal and financial circumstances, these savings shored up consumer balance sheets and created a cushion for the inflation that came later. Government stimulus checks through measures such as the CARES Act also helped consumers make important purchases and pay off debts.

Since then, savings rates have fallen as consumers have spent more dining out, attending events, and on other services. Still, as shown in the accompanying chart, the trend over the past three years is well above average with individuals saving 8.3% of their disposable income. This is often viewed in terms of “cumulative excess savings” – i.e., the total dollar amount that individuals have saved beyond what they typically might – a figure that rose to $2.1 trillion at its peak.

Since mid-2021, these excess savings have fallen as spending has picked back up, declining by $1.9 trillion. Automobile sales have recovered from a low of around 12 million cars per year to 15.7 million recently, dining activity is 23% above pre-pandemic levels, and travel activity has jumped this summer with almost 2.6 million travelers per day. While this spending shrinks financial cushions, it also supports economic growth.

Some investors fear that this trend could result in economic problems in the coming quarters. While there could be a slowdown in consumer spending, this isn’t guaranteed. History shows that there have been long periods during which consumers saved very little, including throughout the mid-2000s. While it’s prudent for consumers to save more from a financial planning perspective, the reality is that savings rates have fluctuated significantly over time – in both good and bad economic environments.

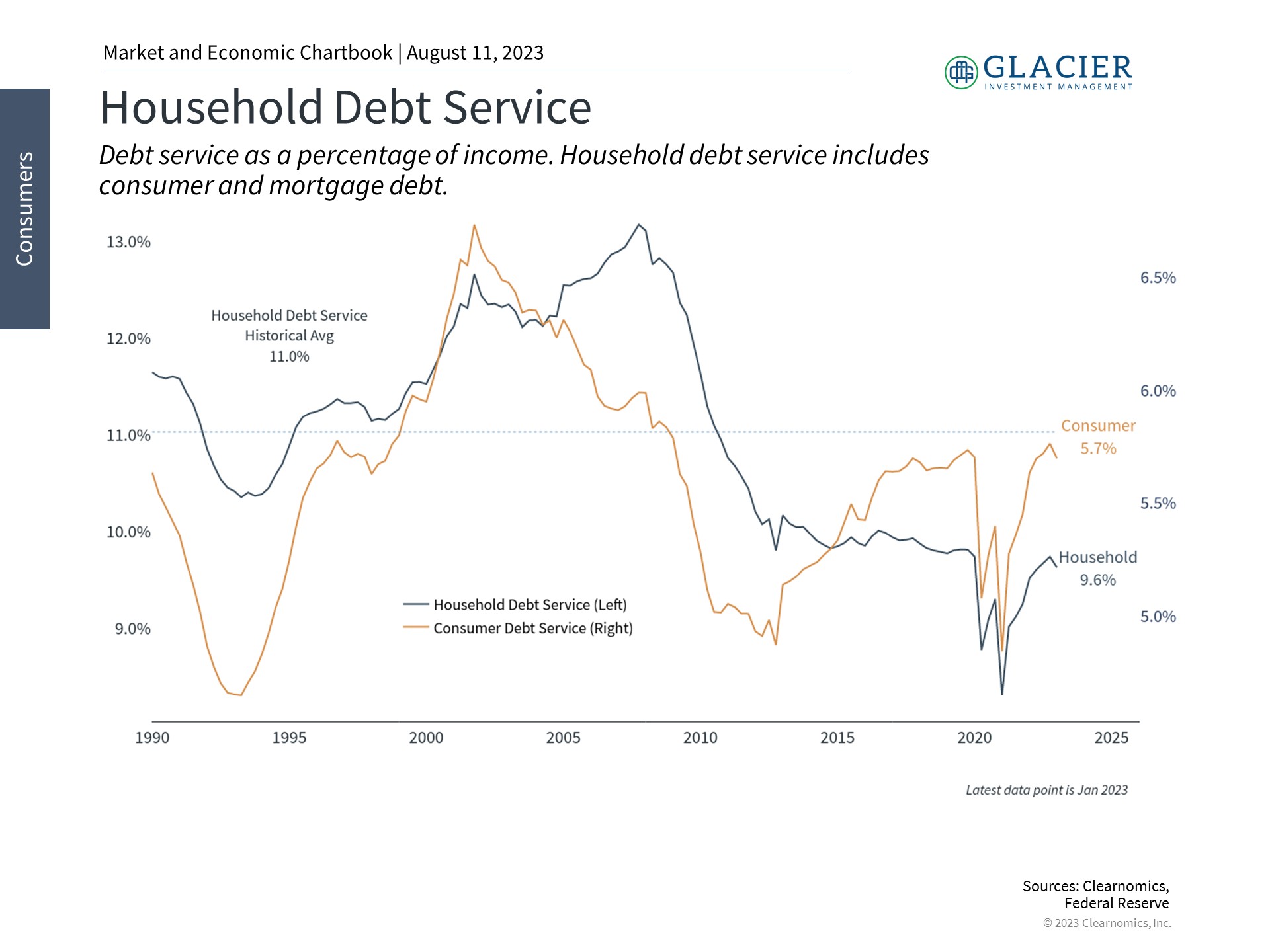

Household debt service has risen but is still historically low+

Additionally, trends such as wage growth due to the strong job market could support both spending and savings. The latest report from the Bureau of Labor Statistics shows that wages rose 4.4% year-over-year. While this has generally been slower than inflation, hourly earnings are still rising at their fastest pace in 40 years. This is happening at a time when the national unemployment rate, at 3.5%, is near historic lows. Job openings have fallen to 9.6 million, but this still represents 1.6 openings per unemployed person across the country.

Other trends have helped to support consumer finances, including the steadily growing economy and this year’s market rally. While household net worth has not yet recovered to its pre-pandemic peak, it reached $150 trillion at the start of the year according to the latest report by the Federal Reserve on the Financial Accounts of the United States.

This is partly because while the aggregate levels of household debt are high across student loans, auto loans, credit cards, etc., what households pay every month is still at reasonable levels. As the chart above shows, debt service levels, with and without mortgage payments, are still below average at 5.7% and 9.6% of incomes, respectively. This is even more true when compared to highly levered periods such as during the housing bubble when debt service ratios were above 13%. Rising interest rates will likely worsen this picture, but this might happen steadily as homeowners benefit from mortgages that were locked in at much lower rates.

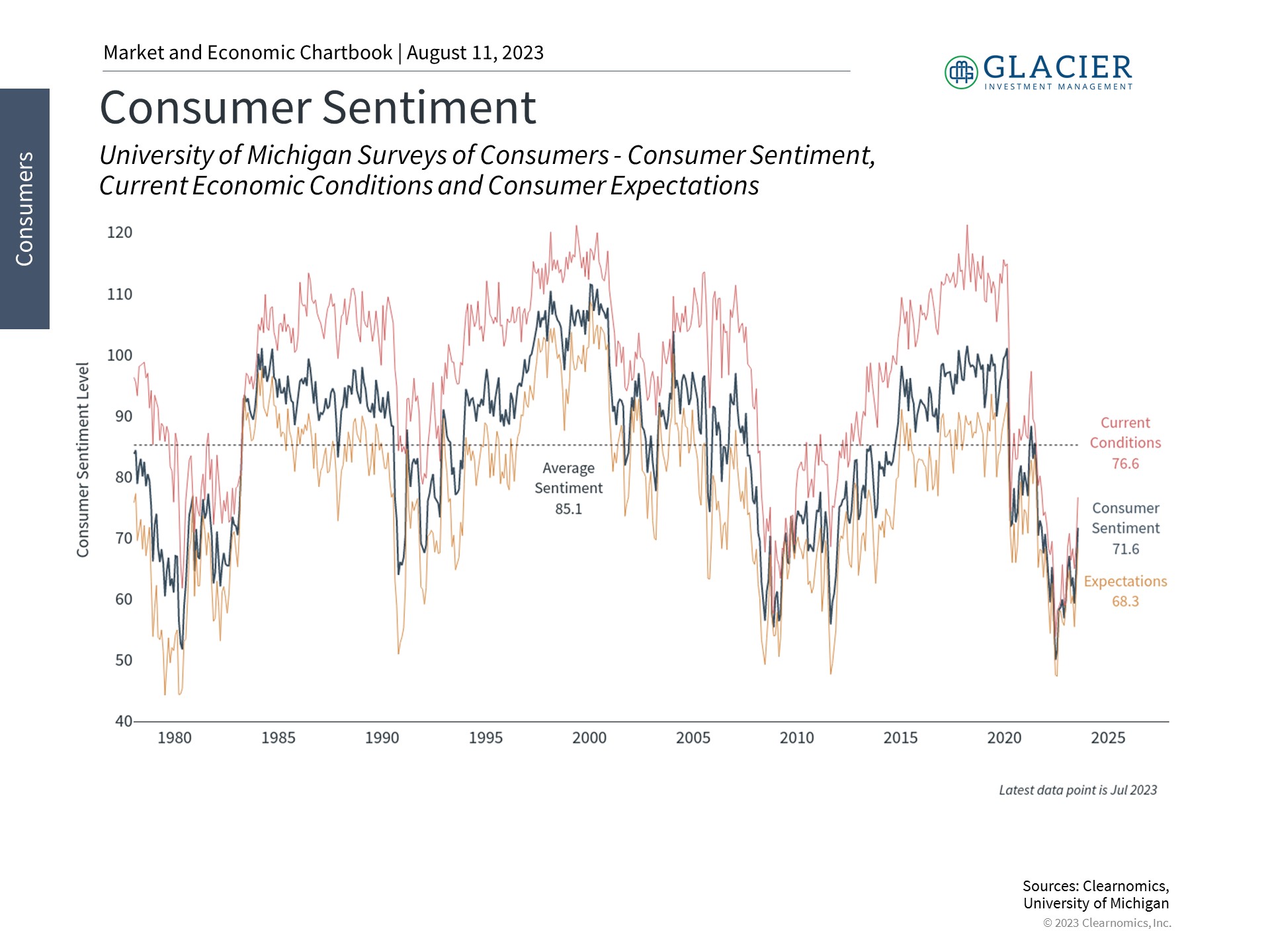

Consumer Sentiment

Of course, how consumers feel can differ from their financial pictures, especially as they look to the future. Consumer confidence, as measured by the University of Michigan Survey of Consumers, has suffered over the past year due to inflation and economic uncertainty. Fortunately, this is slowly improving as the economy stabilizes. According to the same survey, consumers expect inflation of 3.4% in the next year which could then decline to 3% over the next 5 years. While these represent high inflation rates, they are far better than what many had feared even just six months ago.

Consumer sentiment is only slowly improving

The bottom line

Consumers have been an engine of economic growth over the past three years. Although savings rates have fallen, the strong labor market and manageable debt service levels have supported consumer spending and the broader economy. From a financial planning perspective, investors should continue to save appropriately, ideally with the guidance of a trusted advisor, to achieve their long-term goals.