With global growth steadier this year than originally expected, major markets around the world have rallied. The S&P 500 has gained 18% with dividends while developed and emerging markets have risen about 15% and 10%, respectively. Much of the story is due to the relative strength of the U.S. which has served as the main engine of the global economy, just as it did in the decade following the global financial crisis. However, there have been bright spots in other regions as well, at least when compared to what investors and economists had previously anticipated. After all, when it comes to investing, whether something is good or bad is often less important than whether it is better or worse than expected. What’s driving the world economy and why should investors keep a global perspective?

Global growth is better than expected but major regions have diverged

Home Country Bias

It may come as no surprise that U.S. investors tend to focus on U.S.-based investments, especially when it comes to the stock market. This is often referred to as “home country bias” and has been shown to affect the behavior of investors in many countries. For U.S. investors, this has been justified due to the relative strength of U.S. markets and the economy in recent years. Today, the U.S. continues to perform well despite the inflationary concerns of the past year and ongoing Fed tightening. Despite this, investors should not count on this always being the case, especially because portfolios can often benefit from many sources of diversification.

In general, home country bias leads investors to focus on assets with which they are familiar due to geography, rather than what may be attractive and appropriate for their portfolios. This bias doesn’t just stop at countries – investors often show biases toward investments that are even closer to home. The classic examples are investors who primarily invest in hometown companies that they drive past every day, at which they or their friends work, that create the products they use every day, and so on. There is nothing inherently wrong with investing in what you know, but this should only be a starting point. For investors whose primary purpose is to achieve long-term financial goals, it’s important to minimize this bias by understanding where opportunities lie regardless of geography.

One simple way to do so is to understand trends across major geographic regions, especially because investors today have far more access to global diversification opportunities than in the past. Understanding the broad themes across developed and emerging markets does not require investors to be economic or political experts in any particular region or country. Instead, it’s about building awareness around the drivers of each market in order to feel more comfortable investing globally.

For example, it’s easy to understand that Europe has been hit harder by the global shocks of the past few years, especially due to the war in Ukraine which directly impacted energy prices. Growth in the region has slowed across a variety of measures with Q4 2022 and Q1 2023 GDP measures coming in at only -0.1% and 0%, respectively. On a year-over-year basis, the Q1 figure amounts to only 1.1% growth. The chart above shows that Europe’s purchasing manager index (PMI) has fallen into contractionary territory, lower than in the U.S. and China. PMIs represent economic activity across manufacturing and services, where numbers above 50 signal expansions and those below 50 represent slowdowns.

While Europe continues to face challenges, especially in major economies such as Germany and France, it has also been resilient. Inflation improved to 5.5% in June, driven largely by declining energy prices. A milder than expected winter helped Europe maintain natural gas reserves which was a boost to consumers and businesses across the continent. Perhaps more positive is the fact that unemployment has fallen to exceptionally low levels: 5.9% across the European Union. Employment rates are at their highest recorded levels and well above their pre-pandemic peaks. At 81.4% for the Euro Area, the employment to population ratio is higher than even in the U.S.

The dollar has depreciated, driving other currencies higher

Similarly, China has struggled over the past few years but for different reasons. The most recent major shock was the result of zero-COVID policies enforced throughout 2022. This saw major cities, including Shanghai, locked down which hampered economic activity and industrial output. This worsened the supply chain issues that drove global inflation higher, especially for items like computer chips. Also like Europe, there are longer-term worries in China. Demographics are not in the country’s favor as the population ages and declines, and crackdowns on private businesses, especially in tech and education, could hamper innovation and foreign investment. Other problems such as the real estate bubble driven by the “shadow banking” sector and few places to store cash, have not gone away.

More recently, the optimism around China’s re-opening has faded. The latest official GDP report for the second quarter showed that the economy grew 6.3% year-over-year and Beijing recently announced a lower growth target of around 5%. But, once again, it’s all a matter of perspective. The economy’s rebound from COVID lockdowns has been meaningful, as shown in its PMIs. These factors also drove the yuan lower earlier this year alongside many other currencies. While this means that the People’s Bank of China may need to defend the yuan, a weaker currency is a tailwind since it boosts exports and foreign sales. Furthermore, if there is a reversal of the yuan’s depreciation in the coming months or years, it could boost returns on yuan-denominated investments.

Due to its command-and-control economy, investing in China has always been tricky and subject to changing sentiment. However, the relative stability of the economy this year has been positive, despite many sources of uncertainty. This has not stopped the MSCI China index from falling 5% this year (in USD) and the Shanghai Composite index from climbing only 2.4% (CNY). The potential upside is that valuations are now more attractive. In other words, this is not about all-or-nothing investments in Europe or China – it’s about adding diversification opportunities to portfolios as the global economy stabilizes.

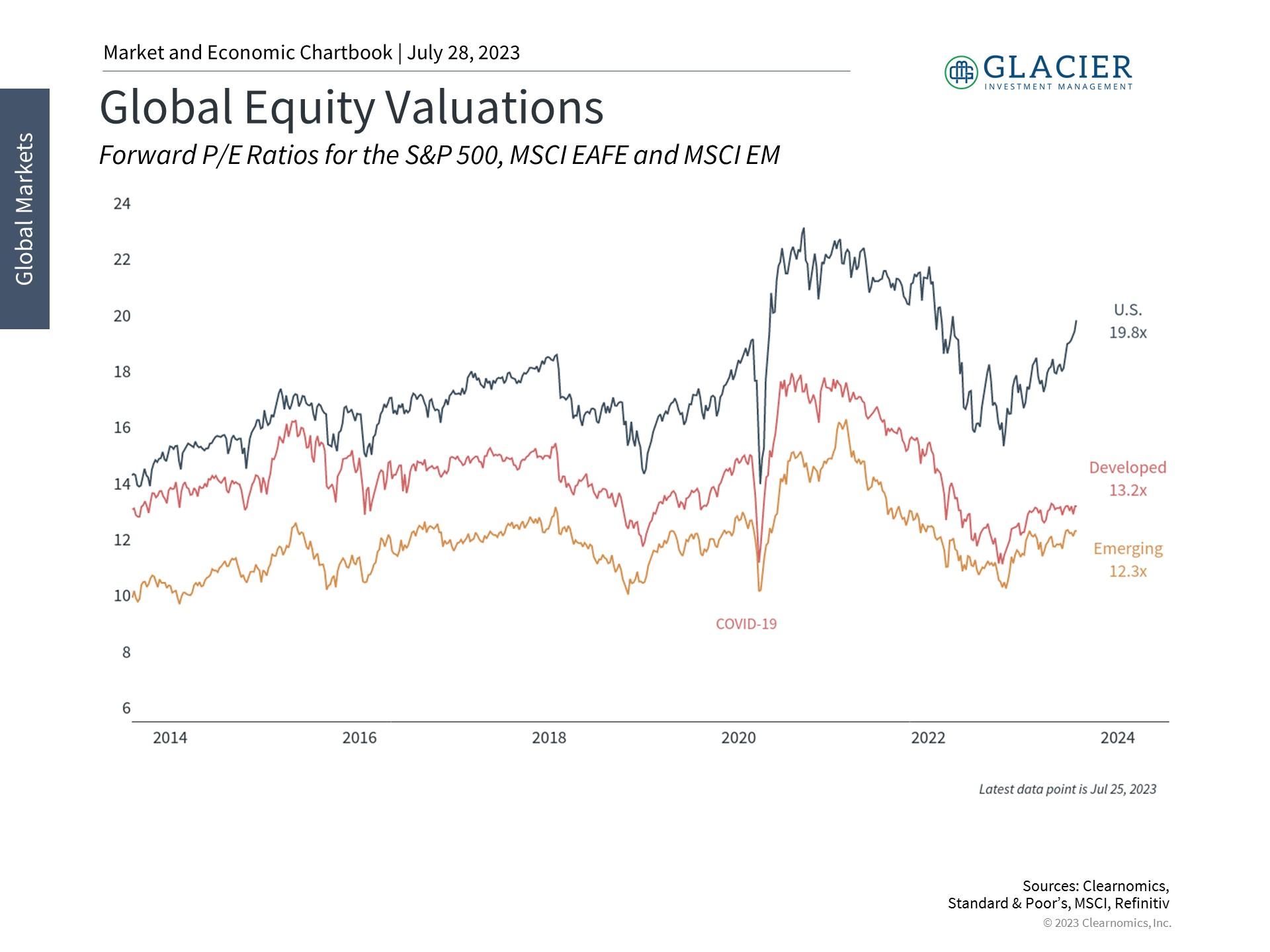

International stocks remain more attractively valued

Just as in the U.S., there are always hundreds of factors, concerns, and issues that investors can focus on in every region. What ultimately matters for investors is not just the balance of risks and opportunities across regions, but how they are valued by the market and how they can contribute to portfolios. Even companies, countries, and regions with mediocre growth prospects can make for sound investments if their prices are attractive enough or their correlations to the rest of a portfolio low enough. Historically, both developed and emerging markets have experienced periods of significant outperformance while providing diversification benefits to U.S. investments.

So, while U.S. stocks are an important component of any diversified portfolio, the accompanying chart shows that international stocks are far cheaper than both the U.S. and relative to their own past valuations. This is partly because U.S. stocks have performed so well this year, raising their valuations to early 2022 levels. Investors who can diversify across regions may be in a better position to take advantage of global growth as world economies continue to rebound from the shocks of the past several years.

The Bottom Line

Investors should minimize home country bias by having a broader perspective on global growth. Doing so can help to improve portfolio diversification as investors work toward achieving their long-term financial goals.