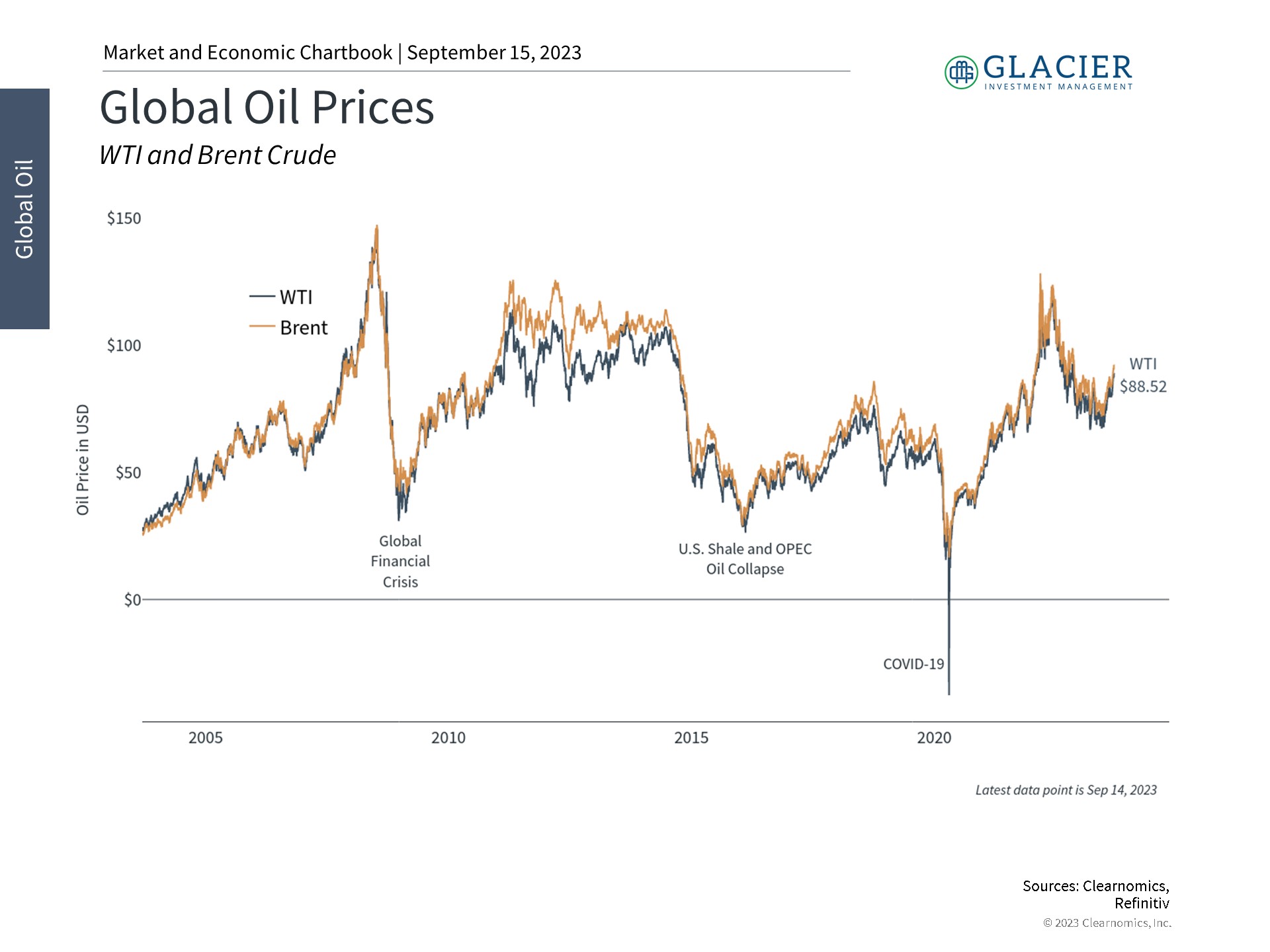

A key driver of global markets and inflation over the past two years has been the price of oil. As an important commodity that fuels the economy, investors watch the oil market closely. While oil has fallen considerably from its peak in 2022, it has also rebounded over the last few months. Since mid-June, Brent crude prices have risen over 26%, from around $72 per barrel to above $90. What do long-term investors need to know about energy prices as the inflation story evolves and the market rally continues?

Oil prices have begun to rise after falling steadily for a year

Oil is still a critical input into economic activity with the International Energy Agency estimating that global demand will rise to 102 million barrels per day this year. Demand plummeted during the pandemic and the price of oil even briefly turned negative, but this reversed quickly as economic growth surged when lockdown restrictions were lifted. Oil prices then spiked in February last year when Russia invaded Ukraine, raising concerns over the supply of energy for Europe and the rest of the world. Fortunately, oil prices began easing soon thereafter, falling from nearly $128 at the peak.

Oil matters to markets and investors for many reasons. Not only does the price of oil interact with broad markets and the U.S. dollar, but it is also an important driver of inflation. Rising energy prices are a direct burden on consumers and businesses who spend more on gasoline and other fuels, putting upward pressure on headline inflation. This also indirectly raises prices on all goods and services as production and transportation costs rise, potentially impacting core inflation. Thus, higher oil prices effectively function as a tax which can slow economic growth and impact corporate profitability.

For these reasons, the recent increase in oil prices could hinder improvements in inflation and act as a drag on the broader economy. Why have oil prices risen in recent months?

The Rise in Oil Prices

First, the U.S. economy has been much steadier than expected. Weakness in oil prices earlier this year partly reflected fears around an imminent recession. The fact that a recession has not materialized, while the odds of a so-called “soft landing” by the Fed have increased, has helped to propel oil prices higher.

Second, Saudi Arabia and Russia recently announced that production cuts of 1.3 million barrels per day would be extended until December. This amounts to 1.3% of global production – not an insignificant sum – and adds to previous cuts. The two countries are among the largest in OPEC+ and have led other cuts in order to prop up oil prices, as well as in response to slower GDP growth and weakness in China. Some economists estimate that this could result in a global deficit of more than 1.5 million barrels per day in the fourth quarter.

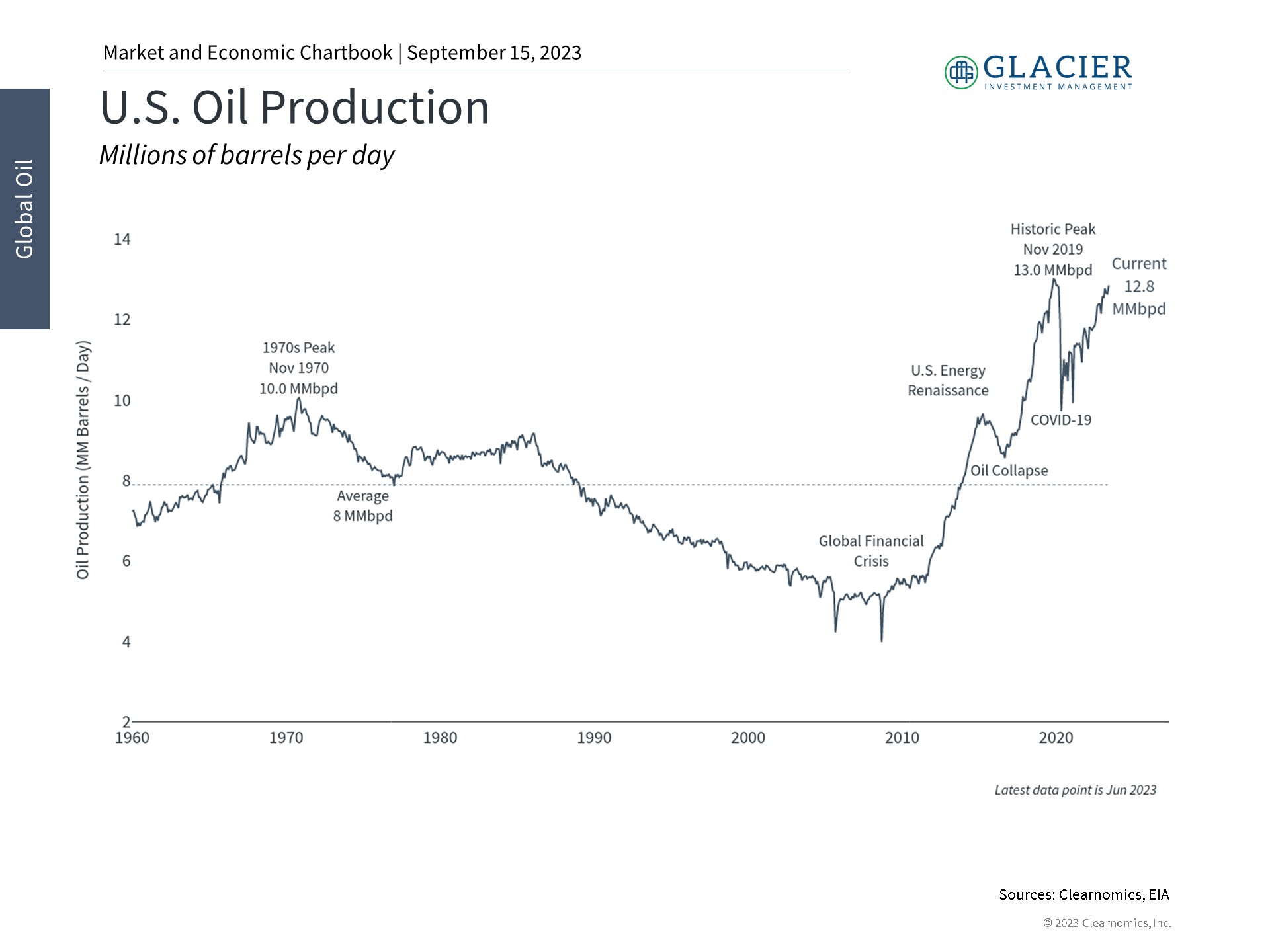

U.S. oil production is returning to pre-pandemic levels

It’s important to maintain perspective around these cuts. The relevance of OPEC as a price-setting cartel has declined over the past decade, partly because cuts by each country are voluntary and difficult to enforce, and because the U.S. has become the top producer of oil in the world. U.S. oil production, as shown in the accompanying chart, is nearly back to its pre-pandemic level of 13 million barrels per day. While there are many nuances in terms of the types of oil produced and consumed in the U.S., Europe, and elsewhere, the fact that the U.S. has been a “swing producer” has shifted the dynamics of the energy markets considerably.

Inventory

Another tailwind for oil prices is declining oil inventories. For instance, the Strategic Petroleum Reserve (SPR), a large emergency supply of oil in the U.S., is at its lowest level since the mid 1980s. This is primarily because oil was drawn from the SPR to offset high prices last year when gasoline was averaging more than $5 per gallon nationwide. The federal government would need to purchase 376 million barrels of oil to restore the SPR to its 2010 peak level. While there is no set timeline for doing so, this deficit naturally places upward pressure on oil prices.

The energy sector has been volatile over the past year

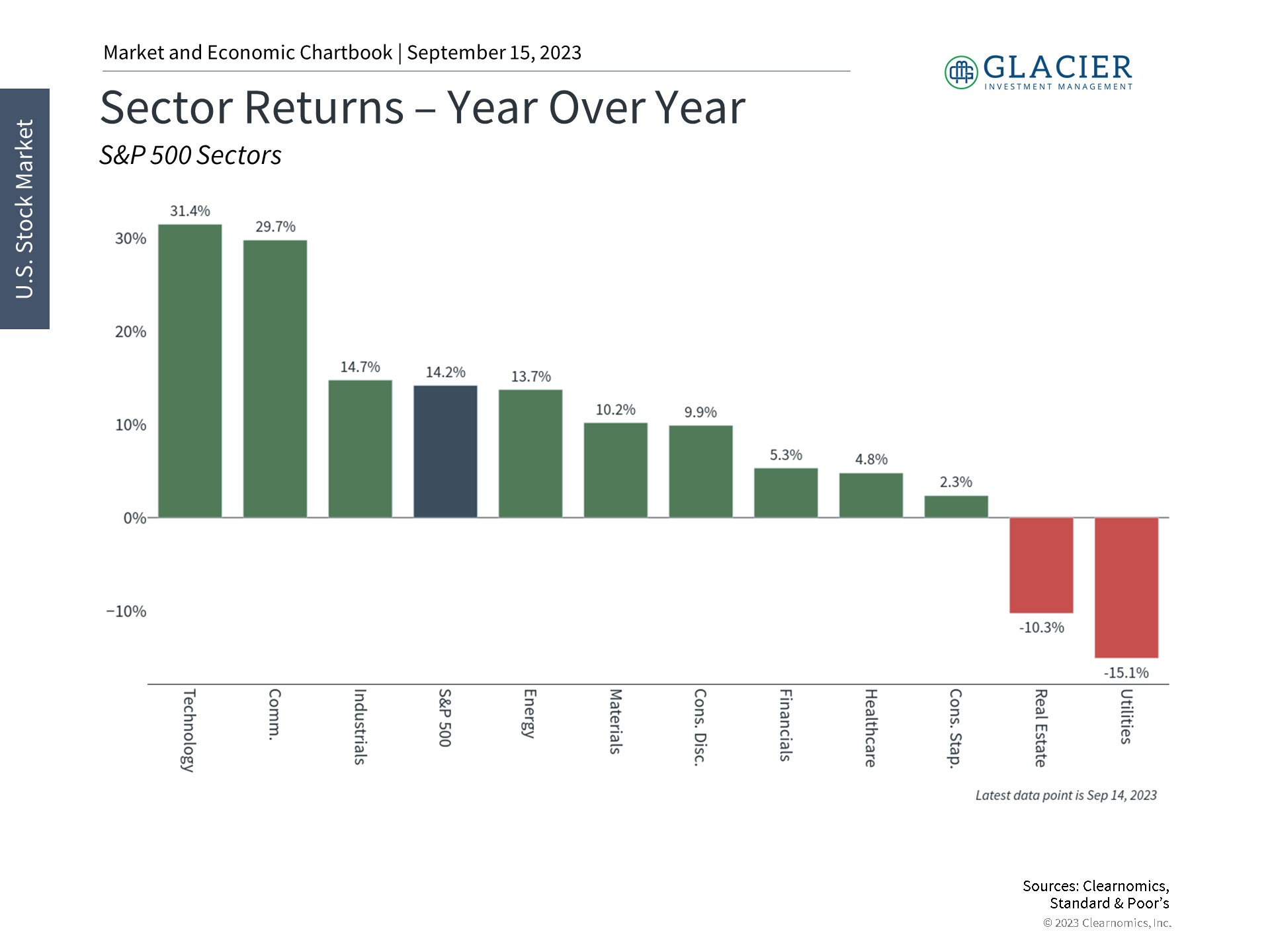

When it comes to the stock market, these dynamics have driven significant volatility for the energy sector of the S&P 500. The sector has risen 17.2% over the past year but this includes a decline of 18.8% from November 2022 to March 2023 followed by full recovery. On a year-over-year basis, its return is third only to the information technology and communication services sectors which have led markets this year. Last year, it was the top performing group.

This is another reminder to investors that it is exceedingly hard to predict which parts of the market might outperform in any given year, and chasing what’s already performed well can backfire as well. Changes in leadership between energy, tech, consumer sectors, and others have been commonplace as the world stabilizes, the inflation story unfolds, and investors look to the next market cycle. As always, the best course of action is simple: long-term investors should maintain balanced allocations across a variety of sectors and asset classes. Doing so in a way that is tailored to financial goals is still the best approach for increasing the odds of investment success.

The Bottom Line

Oil prices have risen in recent months due to a steadier than expected economy and production cuts. While this may act as a headwind, the economy remains healthy and there are other signs that inflation is improving. Investors should stay balanced in the months ahead.